Are women poorer than men?

Investing

|

Jul 30, 2020

According to the Global Gender Gap report 2017, published by the World Economic Forum, “Female talent remains one of the most under-utilised business resources, either squandered through lack of progression or untapped from the onset.”

This affects not only the possibility of you and me achieving financial independence, but puts another hurdle right in our path. Inherently, we as women are seen as lower risk takers when it comes to investments. While this doesn’t necessarily mean that the money we invest won’t grow exponentially, it is definitely a more cautious approach. This means, our money is likely to grow at a slower rate.

Are women risk averse?

A study by The German Institute for Economic Research (DIW) evaluated data on the investment behaviour of more than 8,000 men and women. The study found that 38% of women invested in risky products as compared to 45% of their male counterparts. While the study was left inconclusive, it showed that women were more likely to take more risk, if they earned more, thus concluding that risk and earnings had significant parts to play in a woman’s investment decision making process.

Then why is there such a barrier?

While we cannot say for sure, women tend to fall behind their male counterparts simply because we tend to take more career breaks, and have a higher cost of living. If you thought this was scary enough, we still haven’t spoken about the gender wage gap.

Yes, it exists!

Women are often not seen as equal contenders for a job opportunity and are not seen as people who would stay there for the long term.

Women often tend to pay more than men for similar products including toys and accessories, children’s clothing, adult clothing, personal care products, and home health care products for seniors.

A study that compared 800 products across 90 brands specifically targeting a particular gender showed the following:

Toys and accessories targeted at women/girls were 7 percent more expensive than those targeted at men/boys. The same stood for children’s clothing at 4 percent more for girls, and 8 percent more for adult clothing. A whopping 13 percent more for personal care products and 8 percent more for senior/home health care products.

Closer to home as well, if you pick up a Gillette razor marketed to a man, you would notice that the cheapest razor (for a pack of 5) is priced at ₹ 88.

On the other hand, if you pick up the cheapest razor marketed for a woman, you’ll notice the price at ₹ 80 (for a pack of 1). This is commonly known as ‘the pink tax’, an inherently higher price we pay for a product, just because we are women.

You can perform this experiment across multiple products, shampoos, deodorants, soaps and many more.

How do I stay ahead of the curve?

There are a few things under your control. While you cannot control the cost of things, you can most certainly plan for them. Like for example:

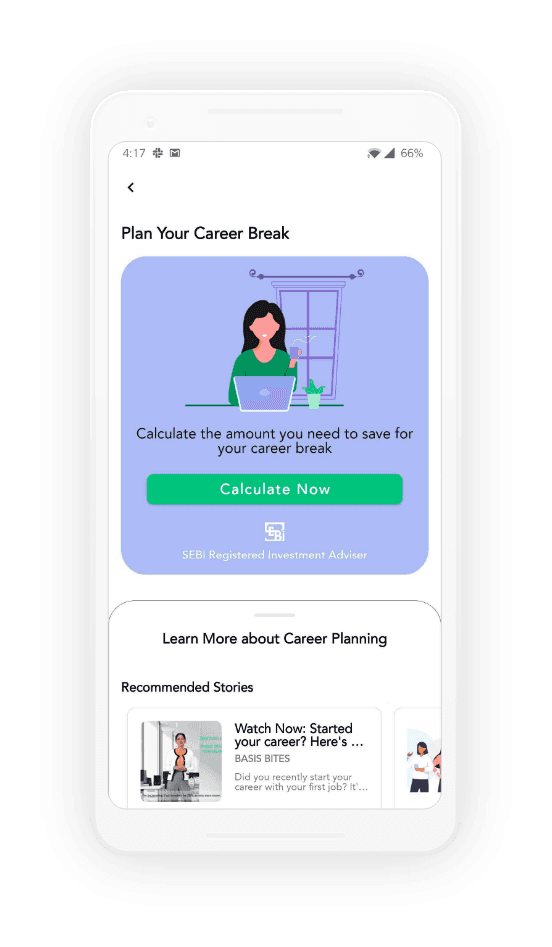

Plan for your career break. We as women know that we might have to take career breaks. One way to get started is to build a career break fund and estimate how much you’ll need. Add a slight buffer to it and you will be all set to start your savings.

If you have a hard time arriving at that amount, you can use the career break calculator at Basis.

This calculator helps you arrive at the estimated amount in just a few simple steps and what’s more, it adds an inflation buffer as well. So you’ll be saving to meet your future costs with ease.

As we grow older, medical health costs and retirement costs such as increase in insurance premiums, purchasing more healthcare and wellness products, grow higher as well. Just as we saw earlier, that senior care products were 8 percent higher for women, keeping up with that is also going to be a task. Another shocking statistic revealed by The World Economic Forum exposed the sad and scary truth of gender pension gaps. The study showed that women generally live around 4.5 years longer than their male counterparts while having to spend increasingly larger amounts on healthcare.

Why is this a cause of concern?

As we live longer and costs pile up, meeting those costs later in life is a lot more difficult than having to plan for them earlier, when you are stronger, healthier and fitter. But saving without a goal is like shooting an arrow in the dark. What if you had an estimated amount in mind? Would that help you control costs better? Absolutely! It is important to know how much you need so that you don’t have to worry about someone else taking care of you later on in life.

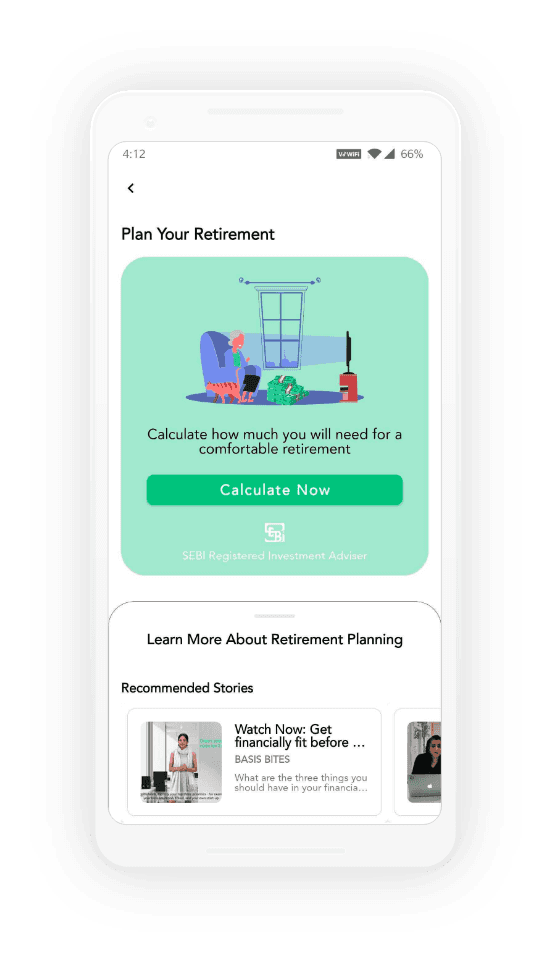

One way you can get started is by creating a retirement plan and sticking to it no matter what. Begin by estimating your retirement corpus. You can do this by using the retirement calculator on the Basis app.

This calculator will help you gauge your current expenses and lifestyle while arriving at an amount that you will be comfortable with when you retire. This way, you can work backwards and build out your retirement corpus.

Nothing in this world is more empowering than having your own money to spend, and save for yourself, just as you please. No strings attached, because you’ve earned it! With so many women working towards their financial freedom, getting started can feel a little intimidating. Which is why we, at Basis have made it our purpose to equip you to ride that wave of financial freedom, with ease!

Basis is a first-of-its-kind platform, aimed at enabling women to achieve financial independence through expert advice, in-app learning modules and supportive communities.

Download the Basis app and live life, your money, your way!

#Worldeconomicforum #women #womenfinance #wagegap #pinktax #wef #equality #womeninfinance #financialindependenceforwomen #womenindependece #careerbreak #retirement

Read More

Unleashing Alexis Rose's PR Magic: Building Her Own Empire

Jul 30, 2020

Unlocking your go to guide to navigate Gold 🌟

Jul 30, 2020

Investing in Gold 101 - A handbook on why, and how to invest in Gold

Jul 30, 2020

Is Taylor Swift REALLY saving the US Economy?

Jul 30, 2020

6 Lessons from The One-Page Financial Plan by Carl Richards

Jul 30, 2020

5 Reasons You Need a ̶P̶r̶e̶p̶a̶i̶d̶ Power Card

Jul 30, 2020